Aviation Cybersecurity Market - By Type, By Deployment, By Threat Type, By Fleet , By Application, By Geography - Global Opportunity Analysis & Industry Forecast, 2024-2030

Aviation Cybersecurity Market Overview

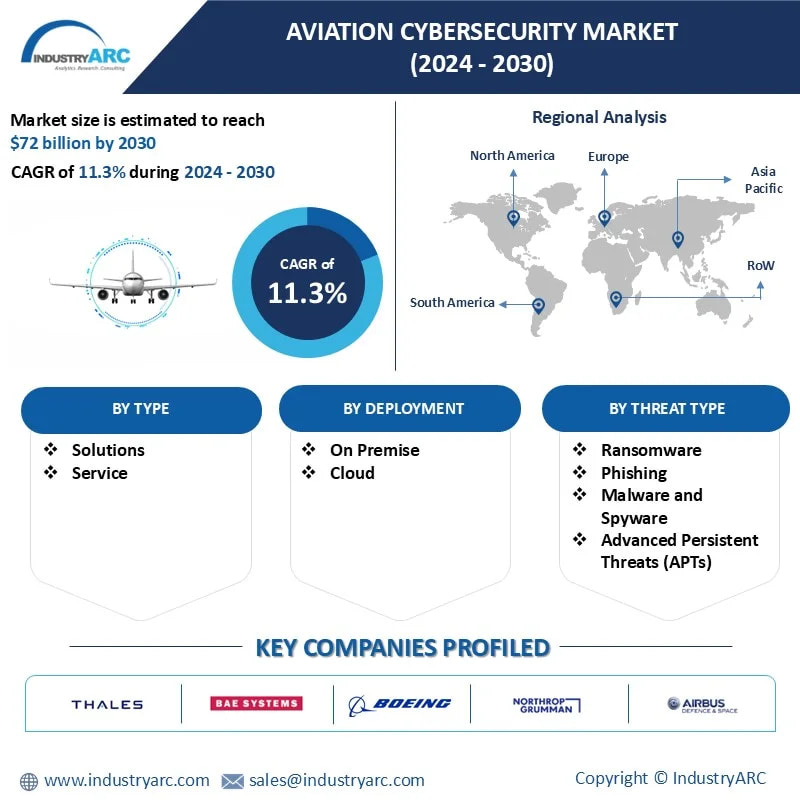

Aviation Cybersecurity market size is forecast to reach US$72 billion by 2030, after growing at a CAGR of 11.3% during 2024-2030. The aviation sector manages a large amount of personal and operational data, on a daily basis, making it a prime target for cyberattacks. Incidents such as data breaches, ransomware and phishing attempts can severely disrupt operations, jeopardize passenger information and compromise critical flight management systems. Implementing robust cybersecurity protocols is essential to safeguard sensitive data, maintain operational integrity and avoid significant financial and reputational damage for airlines and airports. The increasing digitization of aviation infrastructure and the growing complexity of cyber threats facing the industry drives the demand for aviation cybersecurity. Additionally, regulations imposed by national and international aviation bodies mandating stronger cybersecurity measures are pushing airlines and airports to prioritize their cybersecurity frameworks further boosting the market.

A significant trend in the aviation cybersecurity market is the growing adoption of AI and ML to detect and mitigate cyber threats in real-time. AI-powered systems can analyze large amounts of data, identify vulnerabilities and respond to threats before they cause significant damage. Another trend is the integration of advanced encryption techniques to secure data transmission between aircraft and ground control, ensuring the integrity and confidentiality of sensitive operational information. These innovations are shaping the future of aviation cybersecurity.

Market Snapshot:

Report Coverage

The report "Aviation Cybersecurity Market Report – Forecast (2024-2030)" by IndustryARC covers an in-depth analysis of the following segments of the Aviation Cybersecurity market.

COVID-19 / Ukraine Crisis - Impact Analysis:

- The aerospace industry was one of the very first sectors that was affected by the pandemic. As cases surged, governments all over the world struggled to stop the spread of infection and introduced border closures, travel restrictions as a result of which flights were grounded. The aviation sector was hit badly and focused on being operational. Cybersecurity took a backseat as a result.

- The Russia-Ukraine war further emphasized the importance of cybersecurity in the aviation sector. Some cyberattacks against airlines have been motivated by geopolitical issues, with Russia’s invasion of Ukraine causing a big increase in Russian-associated airlines or airports being targeted. For instance, in March 2022, hackers targeted the Russian state-owned aerospace and defense conglomerate Rostec with a DDoS attack on its website.

Key Takeaways

Commercial Aircraft Dominate the Market

Commercial planes represent the largest segment in the aviation cybersecurity market due to the high volume of personal and operational data they handle making them prime targets for cyberattacks. Airlines manage sensitive information such as passenger details, flight operations and financial transactions, all of which require strong protection from cyber threats. A Civil Aviation Supply Chain Cybersecurity Recommendations Report published, in October 2023, by the Aerospace Industries Association noted that civil aviation has an enormously complex and globally connected supply chain. This complexity means that cyberattacks can leave nearly everything in the supply chain vulnerable, right from the data that is used to build physical structures to the software and firmware of complex electronic hardware (CEH) running in products or powering the servers in addition to the electronic hardware itself, as well as the data and production systems used to manufacture structural items. According to Airports Council International (ACI) World’s bi-annual air travel demand update of 2024, global passenger traffic in 2024 is predicted to surpass the 2013 level for the first time since COVID-13, reaching 9.7 billion passengers or 106% of the 2013 level showcasing a 12% YoY growth rate. As the global demand for air travel grows so does the need for efficient and secure digital systems to manage flights, making cybersecurity a top priority for commercial aviation.

Airports are the Largest Segment

Airports are the largest segment in the aviation cybersecurity market due to their role as critical hubs in global air transportation. They manage vast amounts of operational data, handle millions of passengers and operate complex networks of interconnected systems which makes them prime targets for cyberattacks. For instance, on November 13, 2023, hackers executed a Distributed Denial of Service (DDoS) attack on several key Saudi Arabian airports. The affected airports included King Abdulaziz International Airport (KAIA), King Fahd International Airport (KFIA), Prince Naif bin Abdulaziz International Airport and Prince Mohammad bin Abdulaziz International Airport. A group known as Mysterious Team Bangladesh (MTB) took responsibility for the DDoS attacks. Ensuring the security of airport operations, passenger information and air traffic management is essential to avoid disruptions. The growing trends of digitalization further drives the need for stringent cybersecurity measures at airports.

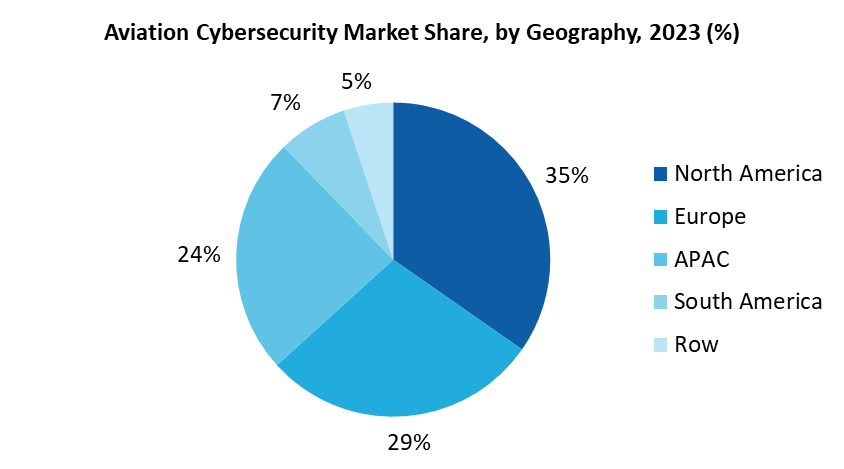

North America Leads the Market

North America holds the largest share of the aviation cybersecurity market due to its mature aviation industry and advanced technological infrastructure. The region is home to some of the largest airlines, airports and aviation technology providers all of which face significant cybersecurity challenges. In November 2023, Israeli aviation cyber security company Cyviation expanded into the United States by opening its first headquarters in New York. The U.S. government imposed strict cybersecurity regulations that drive investments in the sector. For instance, on May 16, 2024, US President Biden signed into law the FAA Reauthorization Act of 2024.The Act reauthorizes and establishes funding for the Federal Aviation Administration and the National Transportation Safety Board through September 2028. Additionally, frequent cyberattacks targeting critical infrastructure in the U.S. have pushed airlines, airports and other stakeholders to adopt comprehensive cybersecurity solutions making North America a dominant player in the global aviation cybersecurity market.

Growing Complexity of Threats and Attacks Fuels Growth in the Aviation Cybersecurity Market

The aviation industry faces increasingly complex and sophisticated cyber threats, pushing the need for advanced cybersecurity measures. Cybercriminals are constantly evolving their tactics from ransomware and phishing attacks to targeted attacks on air traffic control and communication systems. With large amounts of sensitive data such as personal passenger information and critical operational data, aviation systems are becoming more attractive targets for malicious actors. For instance, on December 29, 2023, threat-actor group R00TK1T ISC Cyber Team claimed a successful breach of Qatar Airways. As per the group, they compromised the airline’s ADOC Navigator system for Airbus A330 and A350 aircraft which granted them access to a treasure trove of confidential flight data, maintenance schedules and operational intricacies. Therefore, the growing complexity and scale of these threats underscore the importance of investing in proactive cybersecurity solutions to protect aviation’s critical infrastructure and maintain operational continuity.

Legacy Systems and Modernization of Fleet to Hamper the Market

One of the key challenges for the aviation cybersecurity market is the presence of outdated legacy systems and infrastructure that were not initially designed with cybersecurity in mind. Older systems, for example the ARINC 429 communication protocols used in commercial aircraft prioritize safety and compatibility but often lack modern encryption or protection mechanisms leaving them vulnerable to cyberattacks. In 2018, the U.S. Department of Homeland Security ran nose to tail tests on an aging commercial airliner to detect weak spots and found that the aircraft could be hacked by breaching the plane’s radio frequency communications. Upgrading these legacy systems are expensive, complex and time-consuming as retrofitting older aircraft with modern cybersecurity measures often involves significant changes to hardware and software. This creates a dilemma for airlines which must balance operational safety, cost management and the growing need for cybersecurity improvements.

For more details on this report - Request for Sample

Aviation Cybersecurity Industry Outlook

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Aviation Cybersecurity market. Global Aviation Cybersecurity top 10 companies include:

1. Thales Group

2. BAE Systems

3. Boeing

4. Northrop Grumman

5. Airbus Defence and Space.

6. Cisco Systems Inc.

7. L3Harris Technologies, Inc.

8. RTX

9. Honeywell International

10. Cyviation

Scope of the Report:

Comments

Post a Comment