Emission Control Technology Market – By Technology, By Fuel Type, By Material, By Vehicle Type, By Geography - Global Opportunity Analysis & Industry Forecast, 2024-2030

Emission Control Technology Market Overview

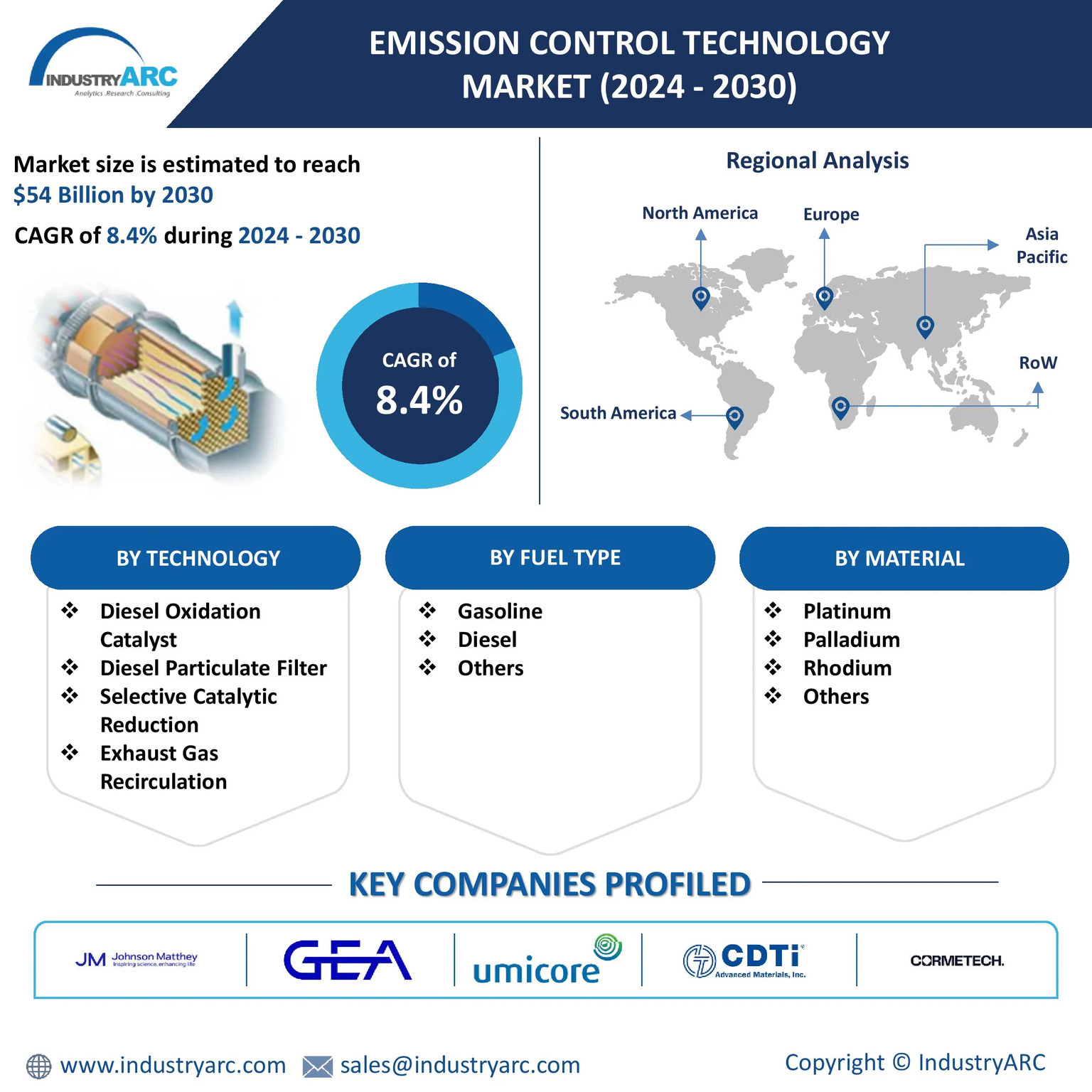

Emission Control Technology Market is forecast to reach $54 billion by 2030, after growing at a CAGR of 8.4% during 2024-2030. Emission control technology refers to a range of techniques, systems, and technologies designed to reduce or eliminate the release of harmful pollutants into the environment. The emission control technology market is driven by government regulations, environmental policies, international agreements such as the Paris Agreement that focus on reducing emissions and the growing public awareness and demand for cleaner and sustainable solutions.

A major trend in Emission Control Technology market is the transition to hybrid vehicles and Plug-in Hybrid Electric Vehicle (PHEV) as these vehicles require different components to manage emissions. As per International Energy Agency’s Global EV Outlook 2024, electric car sales keep rising and could reach around 17 million in 2024, accounting for more than one in five cars sold worldwide. Rise in sales of vehicles worldwide is also a reason for the adoption and development of emission control technologies. Vehicle combustion engines release a variety of pollutants, such as particulate matter, ozone, and other emissions that contribute to smog. As more vehicles are on the road, the impact of vehicles emissions increasing significantly. This has led to stringent regulations which eventually led to adoption of emission control technologies.

Market Snapshot:

Emission Control Technology Market – Report Coverage

The report: “Emission Control Technology Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Emission Control Technology Market.

COVID-19 / Ukraine Crisis - Impact Analysis:

- Air pollution and greenhouse gas emissions were significantly reduced as a result of the COVID-19 pandemic and the countries subsequent restrictions on travel and other economic activities. Stringent restrictions led to reduced industrial activity, lower vehicle usage and a decline in manufacturing. These factors resulted in reduced demand for new vehicles and other equipment which are the primary consumers of emission control technologies.

- A large amount of warming gases have been emitted into the atmosphere as a result of Russia's invasion of Ukraine. Supply chains for essential components required in emission control technology, like semiconductors and rare earth metals, have been disrupted by the conflict. These situations led to delays in manufacturing and rise in cost of emission control technologies.

Key Takeaways

Diesel Particulate Filter is the Largest Segment

Diesel Particulate Filter (DPF) hold the highest market share due to stringent environmental rules. Diesel Particulate Filters serve as a crucial component in modern diesel engine emission control systems. Government emission regulations are raising demand for diesel particulate filters and automotive manufacturing is expanding to support market growth. DPFs are crucial tools in controlling air pollution. These filters are included into the exhaust systems of diesel engines to collect particulate matter (PM), also referred to as soot, which is an undesirable consequence of burning diesel. In March 2024, Environmental Protection Agency (EPA) announced a final rule, Multi-Pollutant Emissions Standards for Model Years 2027 and Later Light-Duty and Medium-Duty Vehicles, that sets new more protective standards to further reduce harmful air pollutant emissions from light-duty and medium-duty vehicles starting with model year 2027. Such regulations are driving the market growth for the diesel particulate filters globally.

Passenger Vehicles are the Largest Segment

On the basis of the vehicle type, passenger vehicles type is analyzed to hold the highest market share in 2024. The rise in sales and production of the passenger vehicles globally is driving the growth of passenger vehicles segment in the Emission Control Technology Market. For instance, as per Society of Indian Automobile manufactures, total passenger vehicle sales increased from 3.07 million to 3.89 million units in FY-2022-23, compared to the previous year. As more vehicles are on the road, the cumulative impact of their emissions becomes increasingly significant. As governments implement stricter emission regulations to reduce air pollution and combat climate change, automakers must adopt effective vehicle emission control technologies.

Europe Leads the Market

Europe dominated the Emission Control Technology market with a market share of 33% in 2023, primarily driven by stringent emission regulations, technological advancements and the region's focus on environmental sustainability. For instance, on 19 April 2023, the European Parliament and the Council amended the regulation to strengthen the CO2 emission performance standards for new passenger cars and vans and bring them in line with the EU’s ambition to reach climate neutrality by 2050. This amendment strengthened the emission targets applying from 2030 and set a 100% emission reduction target for both cars and vans from 2035 onwards. The EU also provided incentive mechanism for zero- and low-emission vehicles (ZLEV) and penalties for excess emissions. If the average CO2 emissions of the manufacturer's fleet exceed its specific emission target in a given year, the manufacturer must pay, for each of its new vehicles registered in that year, an excess emissions premium of approximately $104.6 per g/km of target exceedance. These factors create a favorable environment for the development and adoption of emission control technologies in Europe.

Increase In Automobile Production Boosts the Market

Currently, there is a rise in demand and production of automobile globally. This rise in automobile production globally automatically leads to increased production in demand for emission control technology for emission control devices in automobile exhaust systems. According to a Report By OICA, there is a growth rate of nearly 10.2% in production of vehicles in 2023, when compared with the year 2022. As vehicle manufacturing grows, particularly in emerging markets across Asia and South America, stringent environmental regulations are being enforced to curb pollution and meet international emission standards. Automakers are increasingly integrating advanced emission control systems, such as catalytic converters and particulate filters, to comply with regulations like Euro 6 and China VI. Therefore, increase in automobile production is anticipated to boost the growth of the emission control technology market.

High Cost to Hamper the Market

The initial investment for emission control technologies often includes purchasing specialized equipment, retrofitting existing infrastructure and upgrading processes. These costs can be especially burdensome for smaller businesses and organizations with limited financial resources. The high capital expenditure required upfront creates a barrier to entry, preventing many potential buyers from investing in emission control technologies. Specialized materials like palladium and platinum, which are used in catalytic converters to minimize harmful emissions, are frequently needed for emission control systems. These materials are expensive. For instance, the average catalytic converter has 3 to 7 grams of platinum worth about $100-$237, as per auto nation mobile service.

For more details on this report - Request for Sample

Emission Control Technology Market Key Players

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Emission Control Technology Market. The top 10 players in the Emission Control Technology market are

- Johnson Matthey

- GEA Group Aktiengesellschaft

- Umicore

- CDTI Advanced Materials

- Cormetech

- Ecovyst Inc.

- Nett Technologies

- Cataler

- Tenneco

- Airex Industries

Comments

Post a Comment